WaMu Gave Grandma's Money to Crooks

special announcements

New York Times Reporting on ICT

The article appeared on May 21, 2007.

click here for more info

the short version

a huge security flaw in WaMu checking accounts?

for casual browsers or the short-attention-span crowd

problem

My grandmother was defrauded of nearly $700 by a phone scam. The real scumbags are the "merchants" who scammed grandma and the individuals who work with them. The underlying problem, however, is Washington Mutual's practice of accepting -- unverified -- phone-authorized checks printed up by the merchants themselves in victims', like my grandmother's, name. My grandmother never signed (or even saw) the check they cashed!

goal

I am pressing Washington Mutual (WaMu) to reimburse my grandmother because of their irresponsibility in processing the scammers' check and their laziness in investigating her fraud claim. By doing this, I hope to persuade WaMu and other banks to crack down on criminal scammers, unscrupulous merchants, and insecure business practices. Stop such practices and you'll strangle this breed of scammer. Sure I'd like to get grandma's $700 back, but that doesn't seem likely and it would be reward enough for her if it helped put this scum out of business.

background

My grandma is 80 years-old, well-read, still attends extension classes at her local university, and is nobody's fool. She is not poor but lives in subsidized housing on a fixed income. Her one failing: she was too polite to hang up on a phone solicitor and too trusting to recognize a scam in the making. I am her grandson, a web designer and writer based in Southern California. (And a Washington Mutual account holder myself.)

for the long version, click here

{kind=link}

It does give us both a certain amount of satisfaction to see Washington Mutual seized, frisked, and disgraced. I still have an account with a couple thousand dollars in it with them that I use for some monthly electronic payments but it doesn't sound like that's in any jeopardy.

Good riddance. This blog is over.

New York Times story

Stay classy, Wachovia.

Full article: Papers Show Wachovia Knew of Thefts

Labels: wachovia

That's what you get when you help rip off grandmas. Well, that, and give a home loan to every lying schmuck who walks through the door.

Labels: wamu

Bilking the Elderly, With a Corporate Assist

I'd say that I was happy to see it, but it is anything but happy reading. A great article and I was interested to see that it is the number 2 most popular article on the Times' site today.

The case of Richard Guthrie is just the kind of case I imagined when my grandmother was scammed. I'm very sorry to hear what happened to him and what I can imagine are thousands and thousands like him. I can only express relief that my grandmother didn't end up this far in.

I noticed that the article also reinforces a central thesis of this blog -- American banks and their damned unsigned checks are a big part of the problem:

“Such drafts should be eliminated in favor of electronic funds transfers that can serve the same payment function” but are less susceptible to manipulation, they wrote.

But the Federal Reserve disagreed. It changed its rules to place greater responsibility on banks that first accept unsigned checks, but has permitted their continued use.

More details in the article:

Between 2003 and 2005, scam artists submitted at least seven unsigned checks to Wachovia that withdrew funds from Mr. Guthrie’s account, according to banking records. Wachovia accepted those checks and forwarded them to Mr. Guthrie’s bank in Iowa, which in turn sent back $1,603 for distribution to the checks’ creators that submitted them.

Within days, however, Mr. Guthrie’s bank, a branch of Wells Fargo, became concerned and told Wachovia that the checks had not been authorized. At Wells Fargo’s request, Wachovia returned the funds. But it failed to investigate whether Wachovia’s accounts were being used by criminals, according to prosecutors who studied the transactions.

In all, Wachovia accepted $142 million of unsigned checks from companies that made unauthorized withdrawals from thousands of accounts, federal prosecutors say. Wachovia collected millions of dollars in fees from those companies, even as it failed to act on warnings, according to records.

First time I've heard this mentioned. Rekindles my rage with Washington Mutual, Faye Chapman, Andrew Samuels, and all the banking industry's lackeys. Put the Federal Reserve now at the top of that list.

Still can't figure out why in the hell this antiquated and grossly insecure method of payment is allowed to continue. Other than an ingrained reverence for the status quo.

Labels: wamu

Specifically, he would like to speak to Fred of Integrated Check Technologies, who left a comment here, or anyone involved with ICT (or with companies named Netchex or Payment Processing Center), or who has worked with Thomas Cimicato.

You may reach Charles through the New York Times website or at the number he left here. If you need his email address, email me and I'll be happy to provide it.

As far as my grandma's case:

The bad news is : she never recovered her money and as far as I know. No one was ever brought to justice. Wamu never got back to me. And the banking industry has not changed their practices, meaning some unknown number of people are still getting ripped off by these creeps.

The good news : Grandma hasn't been ripped off since this happened. And I've moved most my money out of my Wamu account into a credit union. (And the New York Times may now be looking into this.)

Labels: wamu

Petro Slams Columbus Firm For Helping Telemarketing Fraud

My question to her: why would they stop the company that was processing the refunds?

Well, in fact, as the Ohio AG's Office press release indicates, this was the company that was taking in the money. I'm sure they were taking in a lot more money than they were giving back -- if they were giving back any at all.

The release notes:

This would explain why my grandma's checks were being cashed in Cleveland. (Ohio is quite the hotbed of corruption.)

Good news -- but then again, I'm sure the crooks behind this are already up and running under a different name. If not, someone's sure to have jumped in their place.

Ultimately, I'm curious to see what kind of sentence, if any, these guys get (if convicted.)

I'm adding them to the watch file:

Integrated Check Technologies (ITP) of Columbus

Check Free Recovery, Inc. of Columbus

Collect-A-Check of Columbus

Ohio Attorney General, Jim Petro

She told me I should have my grandma's bank file an affidavit. When I asked her with whom the bank should file the affidavit, her attitude, which wasn't great to start, soured even further. When I pressed her to explain how this would help, she finally hung up.

If you need to contact CCR, their number is 866-898-7489.

I contacted Wamu to inquire about filing an affidavit, but Andrew Samuel was once more unavailable to take my call. I left him a voicemail asking him to call me back today.

» no response from Andrew Samuel to my follow-up email

» no help from the Office of the Comptroller of the Currency (which oversees banks) or the Office of Thrift Supervision (which oversees Washington Mutual)

I haven't given up, but unfortunately I've been too busy lately to pursue this with any vigor.

A couple other notes:

In response to my post of the email I sent Andrew Samuel at Washington Mutual, someone commented:

He's had plenty of chances. I suspect this is a Wamu troll -- check out complaints on ripoffreport.com and there will usually be someone from Wamu commenting in their defense.

I was reading just now an interesting article in the OC Register on charity scams. Regarding the scam artist's psychology, it notes:

Shover and Glenn S. Coffey of the University of Northern Florida interviewed 45 telemarketers convicted of federal crimes.

They found people who earned $100,000 to $250,000 a year while working just 20 to 30 hours a week. That left plenty of time for "life as party."

"One subject said that they 'would go out to the casinos and blow two, three, four, five thousand dollars a night,'" Shover and Coffey wrote. "Asked how he spent the money he made in telemarketing, one subject replied, 'houses, girls, just going out to nightclubs and lots of blow [cocaine]... lots and lots of blow, enormous amounts.'"

Work itself could be life as party. On the job, many solicitors dressed casually, used drugs and alcohol and got a thrill as potent as any drug from a successful call.

Glad to know my grandma, with the support of Washington Mutual, could help.

The part about not being able to do business in Ohio is interesting. I guess Ohio has already gone after this company.

As with other posts, this is published anonymously with the permission of the person who emailed me:

I recently worked for one of these outfits for two weeks before I was making myself sick being involved. I have absolutely no money and no job either now, but I would rather live in a cardboard box on a street corner than to scam innocent and/or desperate people. I worked on a 'campaign' for Grant Proposals. The company goes out of their way to make it look government affiliated. Upstairs they have another campaign regarding prescription meds for seniors in the USA.

I think what is going on is disgusting.

Clients were having the same problems getting help as you mention. In 8 days I got 8 calls from clients trying to get refunded but having no success in reaching anyone at the 'customer service'.

The other red flag is the Las Vegas, Nevada bit. The campaign I worked claimed the company was out of there. They also claimed to be with the BBB, but all they had done was submit their address. What I later found out was that they had changed the company name and phone numbers, (ostensibly due to problems from scamming with the other names and numbers)

I wish I could sit in a corner there and tell the people who call these places, (i was on an inbound campaign), NOT to believe, trust or give any info to these people. I did find a way to tell many of them they could get better info on gov't grants and help from their local library and librarian. I REALLY wish you luck stopping these scumbags. I think what is going on is dispicable.

If there is any way I could help you, being here in Quebec, I would be happy to. Most of the people who call for these things were in need of Oprah's angel network, not being scammed.

The Company name for the campaign I worked was Liberty First Financial, (but this was a 'new' name for an 'old' scam) I was paid by check from a payroll company called Ceridian, (Ceridian is a legit payroll co. - I recieved my pay from proper businesses who used their services in the past), but the company that hired them to do payroll is just another number company easy to open and close - the current 'number' is 62448837 Canada Inc., 1181 Sainte-Catherine, Montreal, QC H3B 1K4. It is a grey little inconspicuous door behind a guy selling perfume in downtown Montreal. No sign, even on the inside office door upstairs - but, they're there. I would not be at all suprised to find out that this co. is linked to what has happened to your grandma. I think they call themselves y2k or something like that....

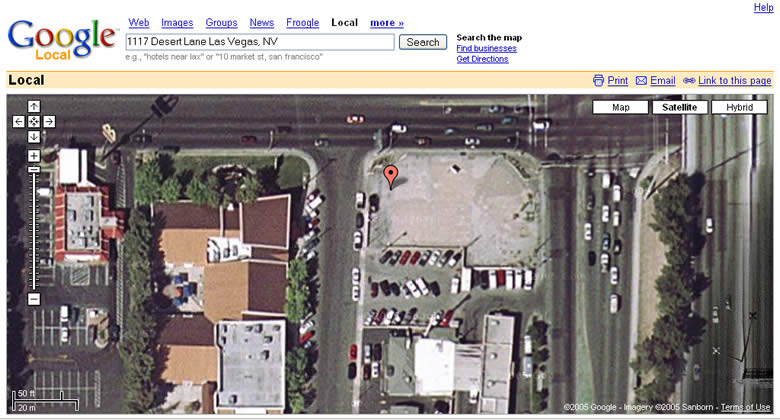

**so i went to las vegas nevada bbb and look-y here what I found:

Liberty First Financial, otherwise known as Priority First Financial

Priority First Financial

(Liberty First Financial)

1117 Desert Ln. #1529

Las Vegas, NV 89102

http://search.bbb.org/

n.b. they are NOT a bbb member (no logo to the left of their name) coincidence? I think not!

**n.b. we were not allowed to do business with OHIO and two other states, (sorry can't remember other two, but I am trying to get in touch with a friend who is still there while he looks for something else - he too is feeling morally guilty for what he is involved in, but does not have the luxury of choosing a cardboard box as living arrangements! If I can get the info I will forward it)

Sincerely,

<withheld>

p.s. please find below links I found of others scammed by Liberty First Financial (postcards sent out as Liberty First Financial, First Liberty Financial and Priority First Financial)

http://www.ripoffreport.com/reports/ripoff186151.htm

http://badbusinessbureau.com/reports/ripoff184283.htm

a couple of these run the same script as what I was given - probably the 'old' name....

http://www.consumeraffairs.com/scam_alerts/grant.html

n.b. by the time i joined they were working an INBOUND campaign (meaning folks called a number on a piece of junk mail). We were told to answer questions of legitimacy by pointing out we had NOT called them, rather they had called us, (but, d'uh, we sent out the postcards) and that we were with the BBB Las Vegas....

I referred the person who wrote me to some state investigators.